We’re here to help

Get in touch

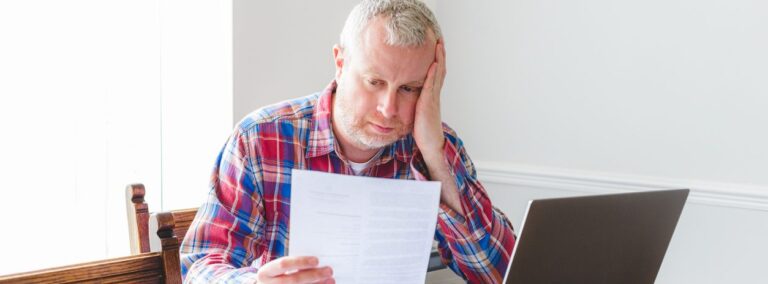

Managing debt can be difficult, but we’re here to help. Our debt relief specialists can show you your options and help you choose the best plan for you.

![Green calendar icon]() Book a consultation

Book a consultation

Leave us your information and one of our specialists will reach out to you.