What to do when you can’t pay your bills in Canada

Bromwich+Smith team

10 Mar, 2026

If you can’t pay your bills, you’re not alone. Many Canadians reach a point where keeping up with payments feels impossible, no matter how hard they try.

Rising living costs, income loss, illness, family changes, or a series of small setbacks can quickly turn manageable finances into overwhelming stress. When that happens, it’s common to feel anxious, ashamed, or stuck, unsure of what to do next.

This article is here to help you understand how to access support when you’re overwhelmed by bill payments and headed towards or in debt.

Feeling stressed about debt doesn’t mean you’ve failed

It means something in your financial situation has shifted beyond what your income can support.

Many Canadians struggle quietly, hoping things will improve on their own. But debt problems rarely fix themselves without action. Understanding that financial stress is common, and often caused by circumstances outside your control, is an important first step.

We want this to be a place of support, not judgment. We are here to give you clarity and direction when things feel out of control.

Signs You’re Becoming Overwhelmed by Debt

Debt often becomes overwhelming before people realize it. Some common warning signs include:

- Missing or delaying payments

- Only making minimum payments

- Receiving collection notices and calls

- Juggling bills to decide which ones get paid

- Relying on credit cards, lines of credit, or loans just to cover everyday expenses

- Using one form of debt to pay another

There are emotional signs too:

- Constant anxiety about money

- Avoiding bank statements or phone calls

- Trouble sleeping

- Feelings of shame or isolation

When debt reaches this stage, ignoring it usually makes things worse. Interest, penalties, and collection activity add pressure quickly. What starts as “tight” can become unsustainable before you have time to adjust.

What Happens If You Can’t Pay Your Bills in Canada?

If bills go unpaid, consequences usually follow in stages.

At first, you may see:

- Late fees and interest charges

- A drop in your credit score

Over time, missed payments can lead to:

- Collection calls and letters

- Accounts being sent to collections

- Legal action, including lawsuits

- Wage garnishment or bank account freezes, including by the CRA in some cases

Understanding these outcomes isn’t meant to scare you. It’s meant to show why acting sooner, rather than later, creates more options and less damage.

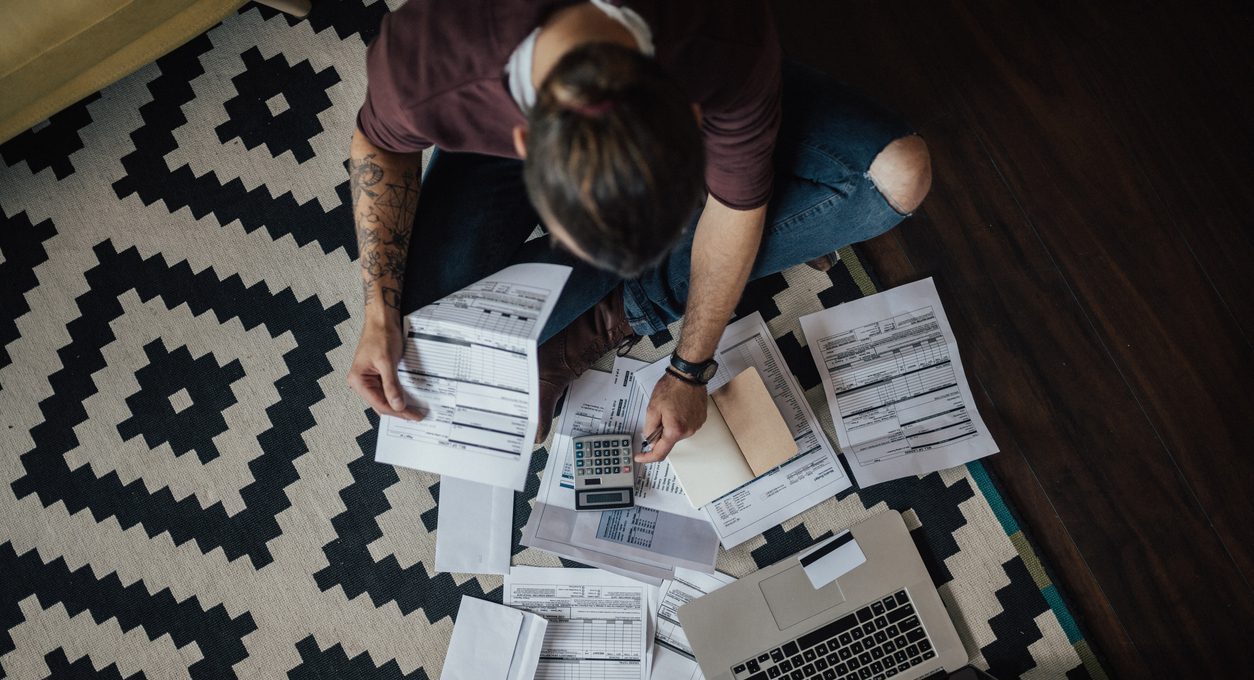

Step One: Stop and Take Stock of Your Situation

When you’re overwhelmed, it’s natural to panic, make quick decisions or become paralyzed and ignore the problem. But the most helpful first step is to slow down and get clear.

Start by listing:

- All debts and balances

- Minimum payments

- Household bills and expenses

- Your current income

It’s also important to understand which obligations are urgent and which can wait. This clarity doesn’t solve the problem on its own, but it gives you control and helps you avoid decisions that could make things worse.

Clarity is the foundation of recovery.

What to Do If You Can’t Afford Debt Payments

Once you can only afford to make the minimum payment or can’t afford payments altogether, the issue has moved beyond budgeting or temporary cash-flow problems.

Missed payments quickly lead to penalties, interest, and creditor action, making it harder to recover without help. This is the point where professional guidance matters most.

Speak With a Licensed Insolvency Trustee Early

A Licensed Insolvency Trustee (LIT) is often the best first step when debt payments are no longer manageable.

Speaking with a trustee does not mean you’re filing bankruptcy or a consumer proposal. A consultation is free, confidential, and focused on understanding your full financial picture.

A trustee can:

- Review your income, debts, assets, and expenses

- Explain all debt relief options

- Help you understand alternatives you may not know exist

- Provide clarity before the situation escalates further

Why trying to survive by borrowing more, delaying decisions, or turning to high-interest credit is a bad idea

Trying to solve your own financial problem alone can lead to:

- Larger debt balances

- Higher monthly payment obligations

- Increased stress and fewer options

Payday loans and high-interest lenders can be especially damaging when you’re already struggling. Unregulated debt advisors and “quick fix” solutions can also cause harm.

Acting Early Creates More Options

Getting help early can:

- Prevent wage garnishment or lawsuits

- Reduce long-term costs

- Give you more flexibility and control

Waiting rarely improves the situation. Taking action does.

When DIY Solutions Aren’t Enough

Budgeting is important, but it doesn’t fix every debt problem.

If debt payments are no longer affordable, DIY solutions often fall short. Debt consolidation loans may not be available or may increase risk. Informal repayment plans may collapse under pressure.

Signs it’s time to explore formal help include:

- Debt growing despite your efforts

- Ongoing reliance on credit to survive

- Collection activity increasing

- Feeling stuck with no realistic path forward

Regulated, professional advice can help you understand what’s possible and what’s not.

Why Debt Stress Feels So Overwhelming

Debt doesn’t just affect your finances. It affects your mental health.

Stress and anxiety can make it harder to think clearly or take action. Shame and fear often stop people from reaching out, even when help is available.

Debt stress is common. It is not a personal failure. And emotional overwhelm is one of the biggest reasons people delay getting support.

Understanding Your Debt Relief Options in Canada

In Canada, the two main federally regulated debt relief options are consumer proposals and bankruptcy.

A consumer proposal allows you to repay a portion of your unsecured debt over time, often with lower monthly payments and asset protection.

Bankruptcy provides legal protection and a full reset when repayment is no longer realistic.

Informal or unregulated solutions can be risky. Federally regulated options exist to protect you and ensure fairness.

How a Licensed Insolvency Trustee Can Help

A Licensed Insolvency Trustee is regulated by the federal government and required to act in your best interest.

A trustee can:

- Explain all regulated options clearly

- Answer questions without pressure

- Protect you from creditor action once a solution is in place

Free consultations reduce misinformation and help you avoid costly mistakes.

Taking the First Step When You’re Stressed About Debt

Taking action early leads to better outcomes. Even a single conversation can reduce stress and restore a sense of control.

Reaching out for help is not a failure. It’s a practical step toward stability.

Clarity alone often brings relief before any solution is chosen.

Get Help If You Can’t Pay Your Bills

Help is available, and it’s regulated.

You don’t have to figure this out on your own. Speaking with a professional can help you understand your options and take back control.

Bromwich+Smith offers free, confidential consultations with Licensed Insolvency Trustees who can review your situation and explain your options clearly.

If you can’t pay your bills and don’t know what to do next, booking a consultation may be the most important step you take.

Frequently Asked Questions About Not Being Able to Pay Your Bills

What should I do first if I can’t pay my bills?

The first step is to stop and take stock of your full financial situation. List all debts, bills, income, and expenses so you understand what’s urgent and what options you may have. If you’re at the point where you can only afford minimum payments, professional guidance can help prevent the situation from getting worse.

Is it normal to feel stressed or ashamed about debt?

Yes. Feeling stressed about debt is extremely common, especially when bills pile up and options feel limited. Financial stress often comes from life events like job loss, illness, or rising costs, not personal failure. You’re not alone, and help is available.

What happens if I stop paying my debts in Canada?

If debts go unpaid, late fees and interest usually increase balances quickly. Over time, accounts may go to collections, credit scores can drop, and legal action such as wage garnishment or bank account freezes may occur, including from the CRA. Acting early can reduce these risks.

Should I take out a loan or use a credit card to catch up?

Using high-interest credit or payday loans to cover existing debt often makes the situation worse. Borrowing to stay afloat can increase total debt and reduce future options. It’s usually better to get advice before taking on more credit.

When should I talk to a professional about debt?

If you can only afford to make minimum payments or are relying on credit to survive, it’s a good time to speak with a regulated professional. A free consultation can help you understand your options before collection activity escalates.

Can debt problems really be fixed?

Yes. Many Canadians successfully recover from debt every year using regulated solutions. While the process can feel intimidating, clarity and the right support often bring relief faster than expected.